Starting with a Mess

Our FIRE assets are currently all over the place. Mr. FireDesired and I have changed jobs a few times over the span of our careers, and each time we basically just left our retirement assets to grow wherever we planted them. I screen-capped a few of them below. It’s a mess.

You’d think that a FIRE-minded couple like us might have paid more attention to this earlier, but the reality is that we kept kicking the can down the road, thinking that we’d work it out eventually. Well, since we’re currently transitioning to a FIRE lifestyle, that “eventually” is now.

ERN SWR SERIES

Wow. I’d heard about the Early Retirement Now Safe Withdrawal Rate Series during our FIRE accumulation phase, but I didn’t realize until now how much information was there. The sheer number of parts to this series is intimidating on its own, and each part seems dense (to me at least). I went through the first three parts (Part 1 ,Part 2 , Part 3), and they simulated a bunch of scenarios that vary equity shares for 30 to 60 year retirements and withdrawal rates between 3 to 5%. The series got me thinking more about capital preservation and equity valuation. After reading these, I was looking at an allocation of at least 80% stocks with a withdrawal rate of somewhere between 3% and 3.25%.

For now, I’ve only read the first three parts of this series, but I plan/hope to go through more of it in the future. I really liked the longer horizon simulations, beyond 30 years. The tables and graphs were awesome too.

ROOTOFGOOD Approach

I’ve always enjoyed the Root of Good blog. It seems to resonate with our own vision of FIRE. I was curious to look at what Justin has been doing. In one of his earlier posts, he mentioned that he switched from about [95% stock / 5% bonds] to [90% stock / 10% bonds]. Then, a few years later, I noticed a comment about going 100% equities with the exception of a 1-2 year cash reserve. But then, a few years after that, he went back to 10% bonds. All of these scenarios on RootOfGood fit in with what I’ve read from the first three parts of the ERN series.

It’s a bit freeing to know that Justin has gone back and forth a bit and still done well.

RETIREBY40 Approach

I peeked in at Joe Udo’s RetireBy40 blog too. He also switched around a bit from 0% bonds before retiring to a goal of 40% by the end of 2019. It’s hard for me to compare ourselves to RetireBy40 because their net worth is so much higher. This higher net worth gives him more of a buffer in tough times to come, so he probably doesn’t need to worry as much about running out of money with a long retirement horizon. And, his wife still works.

Even with the differences between us and RetireBy40, I couldn’t help but take a look as another reference point. I did find this article still in favor of the 60/40 allocation. Interestingly, it was from Vanguard, whose questionnaire Joe used to help determine his allocation in his post.

Our Approach

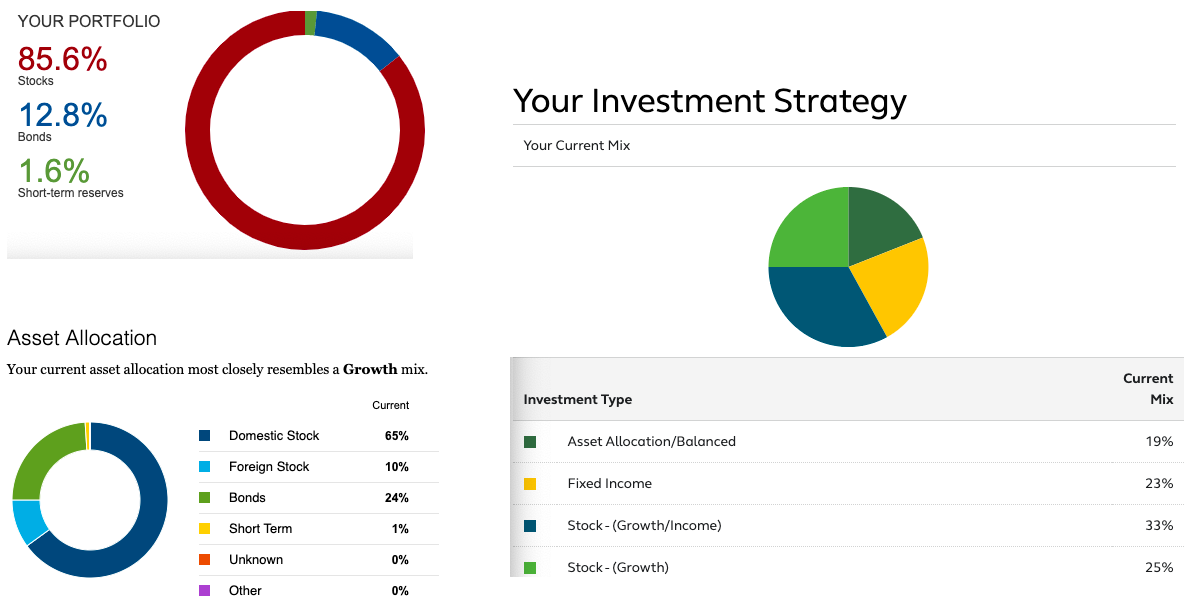

Right now, without doing a full calculation, our assets are roughly about 70% stocks and 30% bonds. We’ve always been conservative, so switching our allocation towards more stocks makes me anxious. However, the simulations from the ERN series and the allocation from RootOfGood persuade me to change ours to an allocation of 85% stock and 15% bonds, at least for this year. Our projected withdrawal rate will be close to 3.00%, which gives us about $48k/year.

I’m sure I’ll churn on this more and revisit it again, at least once a year and probably more. For now, we’re going to try moving in this direction. Our next steps are to go through our taxable and retirement accounts to make sure they are invested as close as possible to our approach.